“Gold soars past $5,100 an ounce, silver hits new record” (The Guardian)

Gold price today: $5,103.10.

Silver price today: $109.06.

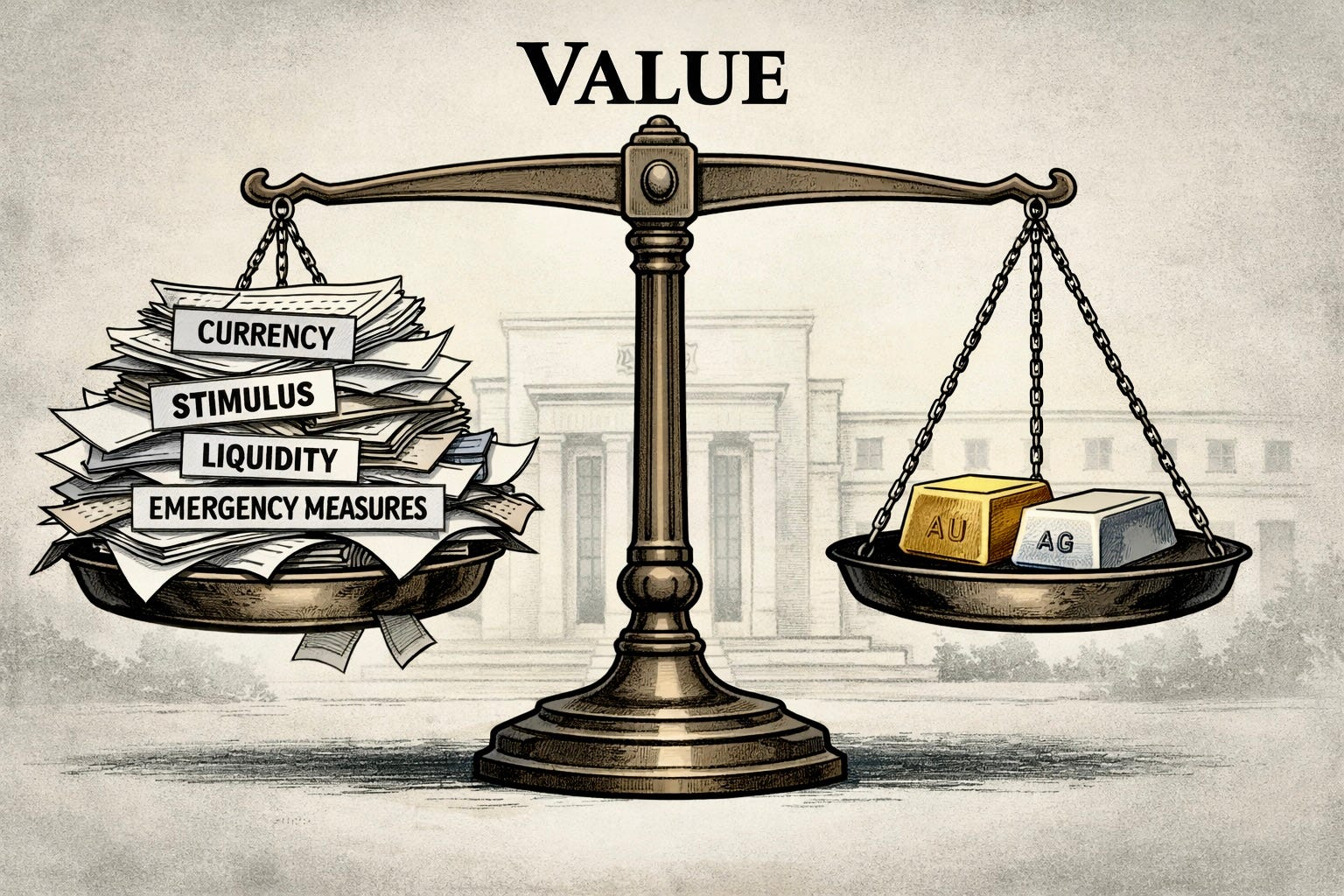

Gold and silver don’t care who’s in the Oval Office. They don’t watch cable news.

They respond to one thing only: Whether the money is still real.

And lately, it isn’t.

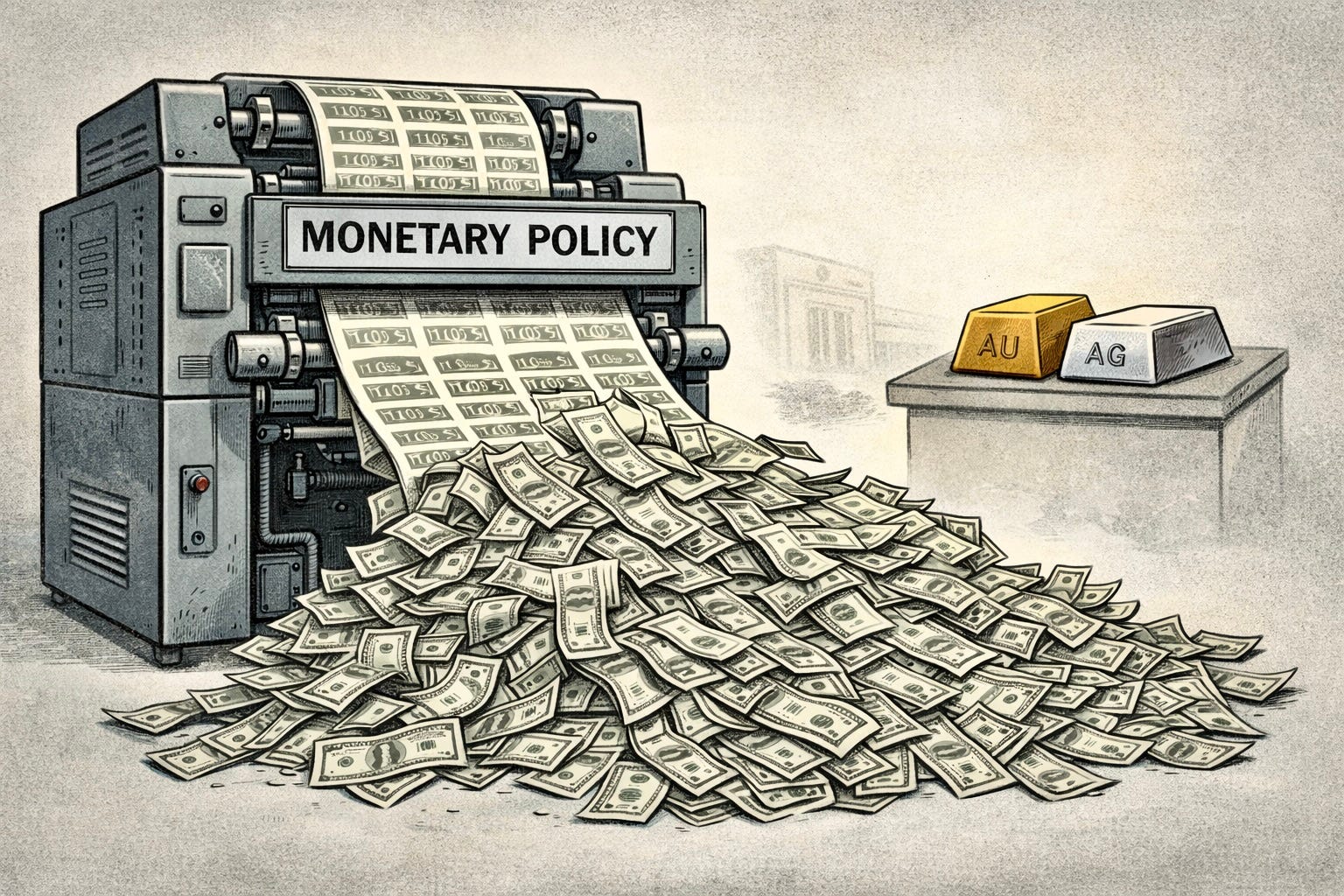

When economists talk about“monetary accommodation” or “liquidity support,” what they mean is this: money is being created out of thin air.

Just keystrokes.

It’s not a conspiracy. That is the system.

Since 2020, we’ve normalized emergency measures as permanent operating procedure. Trillions appeared, balances expanded, debts were absorbed, and the word temporary disappeared from the vocabulary.

We were told not to worry because inflation was “transitory.”

It wasn’t.

Oh, so it was “cooling.”

Uh, no—try again.

Now it’s “manageable.”

Really?

The cost of groceries has doubled, insurance went feral, housing became theoretical— and anyone with a calculator noticed something uncomfortable: The almighty dollar doesn’t go far any more.

That’s where gold comes in.

Gold doesn’t rise because it’s optimistic. It rises because it’s suspicious.

It doesn’t price prosperity. It prices trust.

And trust, right now, is running a persistent deficit.

Gold and silver sit outside the system. They have no issuer. No earnings call. No promise attached. They don’t depend on someone else’s ability to make good later.

They just exist.

And when the supply of money grows faster than the supply of reality, metals don’t rally.

They adjust.

Silver is the more volatile sibling—half money, half industrial input, permanently under-appreciated until suddenly it isn’t.

That’s not speculation. That’s physics.

Debt isn’t repaid honestly. Promises aren’t kept politically. And the system chooses dilution over discipline every time.

Gold isn’t predicting collapse. Silver isn’t screaming apocalypse.

They’re just doing what they’ve always done when currency is lighter than it used to be.

They’re keeping score.

Let’s see how this works by taking a stroll down memory lane.

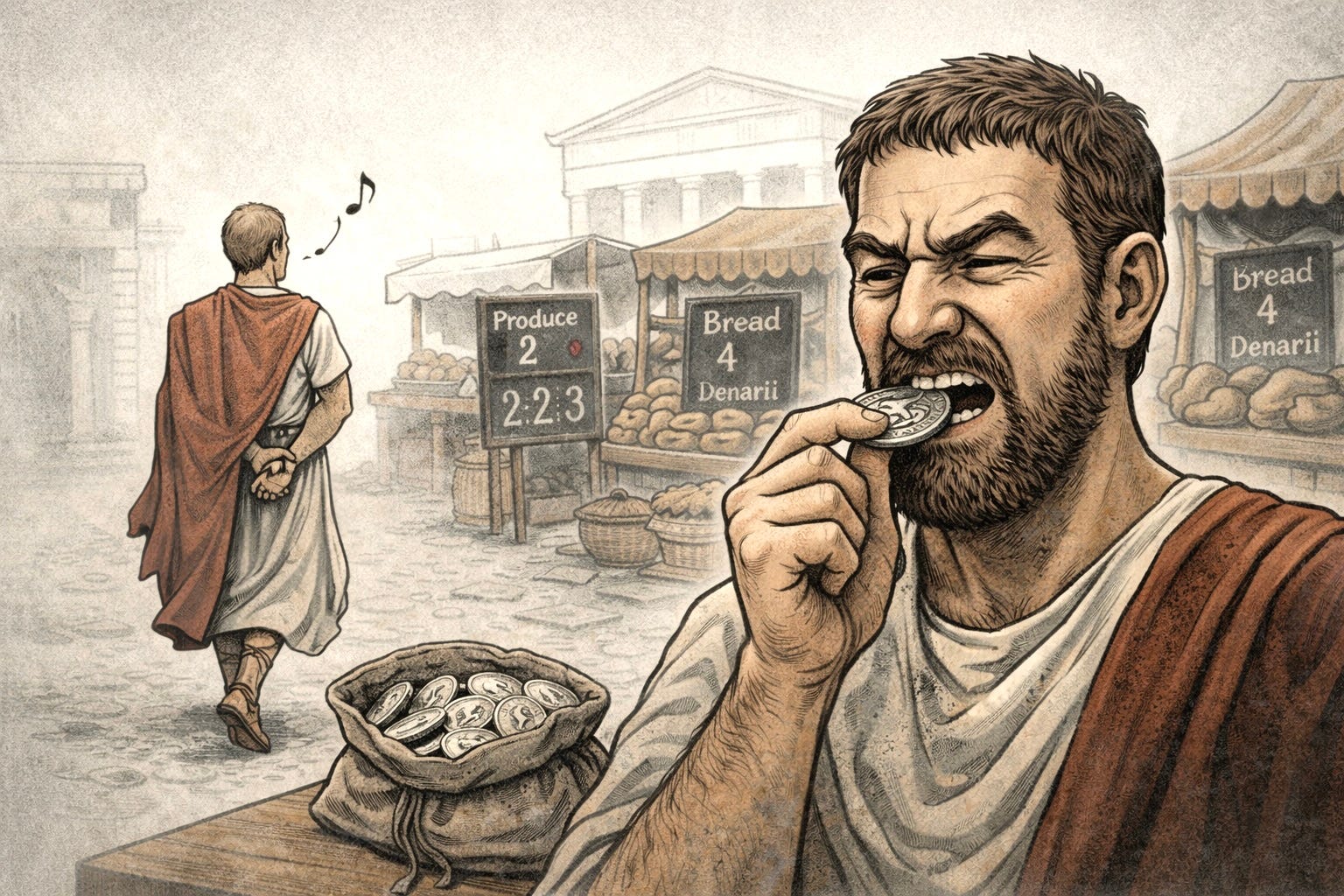

The Roman Empire and Weimar Republic

Early Rome ran on silver coins that actually contained silver. Shocking concept. As the empire expanded, so did expenses—armies, bread, circuses, monuments, corruption.

Eventually someone had a bright idea: What if we keep the coin the same size… but use less silver?

So they did.

And then they did it again. And again. Until Roman coins were silver in name only.

Prices rose. Trust fell. Trade warped. People hoarded older coins and demanded more for goods.

Fast-forward to the Weimar Republic.

Germany had war reparations it couldn’t pay, so they reached for the most elegant solution available: print money.

At first, it worked. So well, in fact, that they printed more.

Currency created with no basis became so plentiful it lost all meaning. Workers were paid twice a day so they could spend wages before prices reset.

Savings vanished. The middle class evaporated.

Enter the Federal Reserve

This didn’t happen overnight. And it didn’t happen by accident.

When the Federal Reserve was created in 1913, the dollar was still tied to gold.

Officially, nothing had changed. Practically, everything had.

The Fed was designed to do three things that gold-backed money resists by nature: expand credit elastically, absorb shocks without defaults, and smooth the political consequences of debt.

Gold demands restraint. Central banking demands flexibility.

The first clean break came in 1933, under Franklin D. Roosevelt, when Americans were barred from owning monetary gold and the dollar was quietly devalued.

Gold still existed—but only for governments.

After World War II, Bretton Woods preserved the appearance of gold backing, but only internationally, and only as a promise. At home, the dollar was already fiat—its greenbacks shifting from “Silver Certificates” to “Federal Reserve Notes.”

Meaning: people could no longer redeem paper for silver.

In the mid-1960s, silver coins began committing an unforgivable sin: they told the truth: The metal inside dimes and quarters was worth more than the number stamped on them. Inflation was leaking out through pocket change.

So Washington fixed the problem.

Silver was removed from coinage. The coins stayed the same size, the same color, the same familiar shape.

Only the honesty was removed.

The final formality came in 1971, when the gold window was closed and foreign convertibility ended.

Gold made promises harder to keep. Silver made inflation visible.

Neither could survive in a system designed to postpone consequences. Not because they failed—but because the system couldn’t live with them.

Once relieved of their official duties, gold and silver went back to what they do best: quietly recording the distance between money as promised and money as practiced.

From 1971 to 1980, gold rose more than twentyfold because discipline had left the building.

So Why Are Central Banks Hoarding Gold Now?

Here’s where it gets awkward.

Publicly, gold is dismissed as a relic and unnecessary in a modern financial system.

Privately, central banks in industrialized countries have been accumulating it like crazy, and without explanation.

They know something the public isn’t meant to dwell on: Gold is the asset of last resort between states. Currency is the asset of convenience within them.

When trust between governments thins, gold thickens.

And Today?

We’re not Rome. We’re not Weimar. It’s not the 1970s.

But we rhyme.

Debt isn’t serviced honestly. Political systems are allergic to austerity. Central banks are trapped between inflation and insolvency.

So the system does what it always does: It dilutes the currency to reduce the real cost of debt. It renames the process to keep it politically survivable. It delays the consequences beyond current decision-makers.

The result?

Gold and silver continue to break new records.

A company named GoldCo tried to get away with selling silver for double its value. You can be scammed many ways when purchasing rare metals.